CAPM and regularized regression

This project focusing the multi-factor CAPM model.

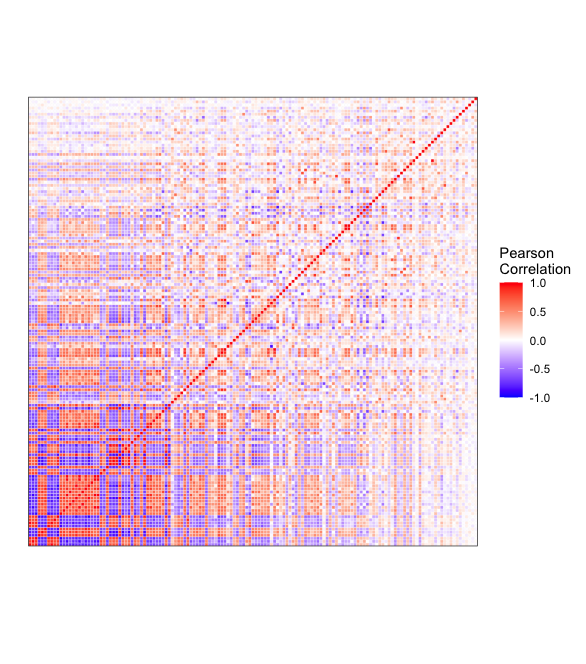

I adopted several linear models and regularized regression models trying to automatically select the best combination of factors for a multi-factor CAPM model based on newly introduced criteria called factor strength.

Packages/Libraries: Tidyverse, lubridate, broom, glmnet, caret, corrr,

Methods/Models: Capital Asset Pricing Model, Monte Carlo Simulation, Linear Regression, Ridge Regression, Lasso Regression, Elastic Net.